Machine Learning Note 1

Coursera 上的Machine Learning 算得上是经典的机器学习入门课程,是由Andrew Ng大牛上的课。出于对机器学习的好奇,打算用Python来完成这门课的学习。

Supervised learning 监督学习

这里存在两种问题 regression 和 classification。前者是预测相关的问题,后者是分类相关的问题。

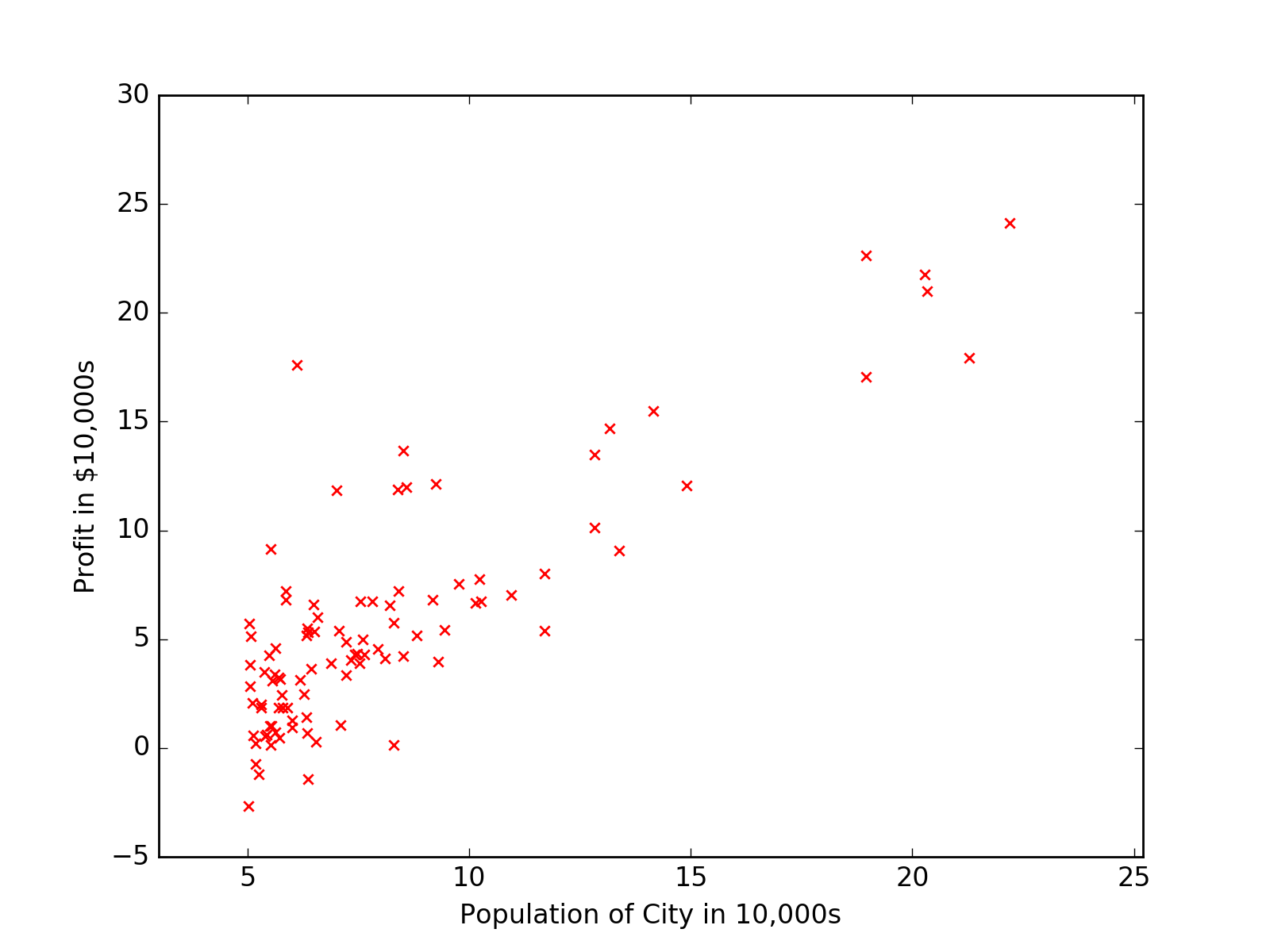

首先介绍的是监督学习,notes1中用房屋价格预测来介绍Linear Regression线性回归。这里因为没有数据集,所以我选择用ex

1中的ex1data1.txt来做演示。

1 | import matplotlib.pyplot as plt |

可以画出数据分布散点图。

机器学习的流程如下

1 | +------------------+ |

用大量的训练数据带入学习算法中进行学习,学习算法产生假设模型,通过假设模型,可以由未知数据X得出需要的Y。

Linear Regression 线性回归

根据 ex1data2.txt 里的数据,因为有两个特征,所以可以写出假设模型

$$ h_{\theta } = \theta_{0}+ \theta_{1}x_{1}+\theta_{2}x_{2}$$

其中 $\theta_{i}$ 是线性方程的确定性参数(有点类似权重的东西?)。所以,假设 $ x_{0} = 1$, 从广义上可以定义假设方程

$$h_{\theta } =\sum_{n}^{i=0}\theta_{i}x_{i}=\theta^{T}x$$

其中 $\theta$ 和 $x$ 都是向量,$n$ 是输入变量的个数。

确定完假设模型,之后需要做的一件事是挑选学习 $\theta$。一个可靠的方法可以让 $h(x)$ 接近 $y$。为了评估假设模型与数据集的接近程度,定义了一个 cost function(代价函数)

$$ J(\theta )=\frac{1}{2}\sum_{m}^{i=1}(h_{\theta}(x^{(i)})-y^{(i)})^{2} $$

这是least-squares cost function,是 ordinary least squares regression model 的一部分。

LMS algorithm

为了寻找合适的 $\theta$ 使 $J(\theta )$ 最小,可以使用LMS算法通过不断的改变 $\theta$ 来寻找合适的值。这里使用了 gradient descent algorithm(梯度递减算法),更新 $\theta$ 的方式如下

$$ \theta_{j} := \theta_{j} -\alpha \frac{\partial }{\partial \theta_{j}}J(\theta) $$

其中,$\alpha$ 是 learning rate(学习率), $\frac{\partial }{\partial \theta_{j}}J(\theta)$ 可以化简为

$$ \frac{\partial }{\partial \theta_{j}}J(\theta) = (h_{\theta}(x)-y)x_{j} $$

这样的更新规则称为LMS update rule(least mean squares),也称为Widrow-Hoff learning rule.

$$ \theta_{j} := \theta_{j} + \alpha (y^{(i)} -h_{\theta}(x^{(i)}))x_{j}^{(i)}$$

梯度递减这里提到了两种 batch gradient descent (批量梯度递减) 和 stochastic gradient descent (随机梯度递减)。